Visa has established a new

strategic agreement with Western Union, a global leader in cross-border,

cross-currency money movement.

Western

Union will implement Visa Direct – Visa’s real-time push payments

platform – to bring speed and transparency to the process of sending

money around the world.

“Together, Visa Direct and Western Union are collaborating with plans

to scale real-time cross-border payments to businesses and consumers in

more than 200 countries and territories, in more than 130 currencies,”

said Bill Sheley, global head of push payments at Visa.

Once Western Union’s implementation of Visa Direct is live, Western

Union will be able to offer customers an expedited remittance service

onto cards with more transparency and an enhanced user experience for

both senders and receivers.

“Western Union has the largest money transfer retail network and this

agreement represents a key milestone for our account pay-out network

combining the best of Visa and Western Union’s cross-border capabilities

to enable a world-class payments platform,” said Jean Claude Farah,

executive vice president at Western Union.

In 2018, Western Union completed more than 800 million transactions

for consumer and business, as nearly $80 trillion of money is sent via a

wire transfer or bank account globally daily. However, the process is

hard and complex, with money taking days to arrive, caused by outdated,

multi-step, costly methods.

This collaboration reinforces Visa’s commitment to modernise how

payments are made around the world. In addition to this new

collaboration, last month Visa announced the acquisition of control of

Earthport, a company that provides cross-border payment services.

The acquisition of Earthport is an extension of Visa’s overall cross-border strategy that’s complementary to Visa Direct and Western Union’s existing partnerships.

What should banks and credit unions do about their branches? A recent Celent report, sponsored by Reflexis Inc.,

an workforce management firm, notes that there is broad agreement that

priority tasks include improving branch sales performance, taking the

customer experience to the max, and adopting “digital advocacy” — using

branches to educate consumers about how they can bank digitally.

However, while many institutions understand those goals, often they

aren’t equipping their staffs with the kinds of tools that will help

accomplish them, according to the latest in a series of projects Celent

has pursued regarding the future role of branches.

Banks and credit unions “are asking front-line staff to deliver

highly personalized customer experiences without the tools to do so,”

Celent states in its report, “and are asking managers to orchestrate

complex systems of personnel and processes without an adequate

understanding of what’s happening across the network.”

This comes at a time when the attitude of banks and credit unions

regarding branches increasingly is in a state of flux. Bob Meara, Senior

Analyst at Celent, says in an interview with The Financial Brand

that for all the talk about the branch being dead, study after study

indicates that many consumers still haven’t warmed up to mobile banking.

“They don’t understand that there’s a tsunami coming, because it still looks like a nice day outside.” — Bob Meara, Celent

Institutions have been trying out all kinds of variations on staffing

and service models — typically with multiple templates within the same

organization. Half of institutions over $10 billion in assets told the

firm that they are in the midst of evolving towards new branch staffing

models, while one in five institutions under $10 billion are doing so.

Yet some institutions still just seem stuck.

“Digital advocates are zealous proponents of what they believe, and

they see the world through that filter,” Meara states. On the other hand

he finds that many executives responsible for branch systems “see

things through a lens of a very different color. Some are very

dismissive of what’s happening on the digital side.” Meara isn’t a

digital-only advocate, but he believes these executives are being

short-sighted. “They don’t understand that there’s a tsunami coming,

because it still looks like a nice day outside.”

( sponsored content )

A Credit Union’s Lesson When Members “Checked In”

When Meara was wrapping up his research, he held a conference call. A

small credit union told listeners that it had recently begun asking its

members to check in on a tablet when they arrived at branch, recording

the reason for the visit. Management was surprised when the most common

purpose given was to have something notarized.

The credit union reacted by training more staffers to be notaries.

Until the tablet check-ins, the employees hadn’t noticed that the demand

to notarize documents was so great that members were leaving because a

notary wasn’t available.

“I wondered, ‘How could that possibly be?’,” says Meara. “But it’s true.”

Notary service isn’t even a loss-leader. Typically it’s solely a

courtesy service that fulfills a key consumer need. But the story

illustrates a key point. Over the course of his project, “Managing

Today’s Branches with Yesterday’s Tools,” Meara found that as banks and

credit unions continue to debate the role of branches versus digital

channels, they frequently do so without suitable data.

“Digital channels represent an information-rich environment,” says

Meara. “You can tell exactly where consumers come onto your website, how

they move throughout the site, where they jump off, where they

encounter problems, and where they find broken links. All that data can

be super-useful.”

On the other hand, many institutions face multiple gaps when it comes to knowing what’s going on in their branches.

“If you ask branch bankers about the details of their teller

transactions, they can wax eloquent about those metrics,” says Meara.

“They can tell you the average number of teller transactions in a branch

and even where the peaks and troughs are.”

What is less-often tracked and measured, Meara finds, are factors of

current branch activity that relate to what many regard as the

increasingly dominant role of branches, as sales and service locations,

and regarding the quality of the customer experience.

In this webinar from Kasasa, you’ll also learn how to achieve higher

ROI with multi-channel marketing by leveraging data, and much more!

Thursday, June 27th at 2pm EST

What Branch System Management Misses

Celent’s research found that many institutions seem confused about

what makes for a good branch customer experience. A strong stress is

being put on personalized service, for example, and on sales results,

while convenience-oriented matters, such as reducing waiting times and

differentiating through offering the most convenient hours — which can

influence sales — rank lower in priority.

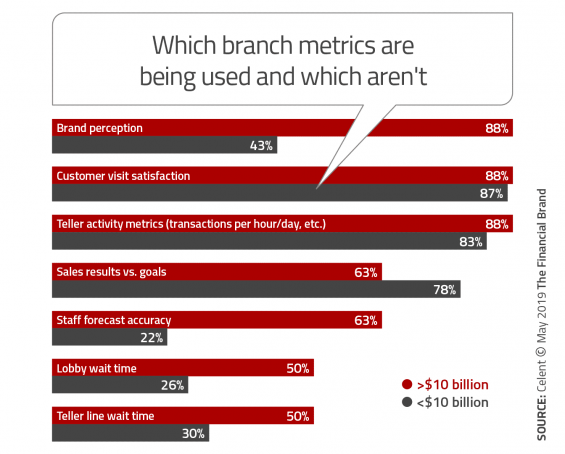

The study found that many banks and credit unions — most notably

those under $10 billion, though not exclusively — lack a clear picture

of key elements affecting the customer experience. For example, as seen

in the chart below, while almost nine out of ten institutions of $10

billion-plus measure overall brand perception, over half of those

institutions under $10 billion don’t track this. Teller transactions are

well tracked, but the report says that with more routine activity going

digital, such measures are less and less relevant.

Lobby and teller line waiting times would be much more important to

ascertain, the report suggests, and many fewer institutions track that.

Meara raises another point: “Many institutions are falling all over

themselves to perfect the mobile experience for consumers,” says Meara,

but they aren’t always striving to do so on the branch front.

By comparison, what makes Apple Stores more than popup showrooms is

the Genius Bar all the way in the back, where the perplexed can obtain

clarity and the desperate can obtain resuscitation for their digital

devices.

What consumer today wouldn’t like to have the assistance of a

qualified “Digital Banking Genius”? Yet Celent found that 55% of

institutions surveyed don’t staff for such positions at all. One in ten

provides a “genius” or a “digital advocate” in all branches, and 35% use

them in some locations.

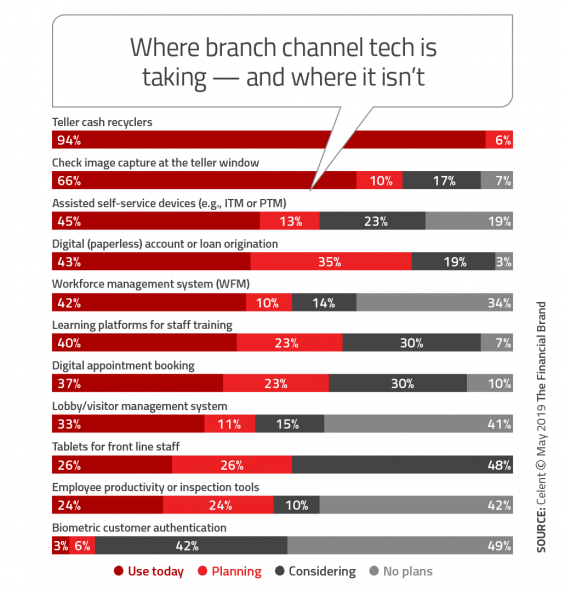

Workforce management systems would help branch officials better

manage service quality, but often these aren’t used. As shown in the

chart below, while four out of ten institutions use such software

currently, 34% don’t — and have no plans to do so. Another 10% are

planning to adopt the software and 14% are thinking about it.

“Such software, sets a baseline for having the right people in the

right place at the right time,” Meara states. He points out that with

limited staffs institutions should be thinking more in terms of

optimizing the customer experience with the staff they’ve got, he says.

One aspect of that is cutting the time that branch staff spends on

tasks that remove them from consumer contact. The report found that

minimizing non-contact time was a lower priority for many institutions

under $10 billion — somewhat surprising given the community banking

mantra of “great service.” Over the entire sample, two out of three

respondents thought that activities taking branch staff away from

customers and members “are either not a concern or not a problem needing

a solution.”

This astounds Meara, because for about a third of institutions

polled, the equivalent of a day’s time is spent away from customers and

members each week.

“If I were a banker, I’d want to know exactly how each frontline

employee spends their day. I don’t mean that from a Big Brother

standpoint, like knowing who’s checking Facebook on company time, but

how much time they spend selling, how much advising, versus time spent

on compliance, and administrative tasks,” he explains. “In many banks,

personnel is roughly half or more of total operating costs. So I would

want to know when someone comes to the branch and leaves without having

their needs met.”

“I would make that the first thing I saw on my desk every morning,” Meara stresses.

Institutions Aren’t Investing in Modern Branch Tech

Only a small portion of institutions surveyed are investing heavily

in technologies that could help optimize use of costly human staff in

branches and simultaneously improve the customer experience.

While some tech is widely used, such as teller cash recyclers, usage

falls off quickly with other tech that could help. Digital appointment

booking is only used by about a third of institutions surveyed and only a

quarter of institutions equip frontline staff with tablets, for

example.

In spite of branches’ importance to sales, Meara says that many

institutions fail to use sales data to reach conclusions about what

works and what doesn’t, and how to match good salespeople with those who

need coaching.

“It’s not for lack of awareness of these tools,” says Meara. “That

much we know.” Nor are institutions being cheap. “I just don’t think

they are appreciating the value and importance in investing in some of

these technologies.”

Legacy Practices Drag as Much as Legacy Computing

Some executives questioned for the study complained about competition

with new channels. Meara noted that the head of ATM services for one of

the largest banks in the country said to him, “Bob, I’m competing with

the digital people for funds, and I get no respect, I’m just the ATM

guy.”

“Maybe there is a little bit of ‘woe is me’ there,” says Meara. “But

branch and ATM channels don’t get the priority of digital channels

anymore except maybe in some really small financial institutions.”

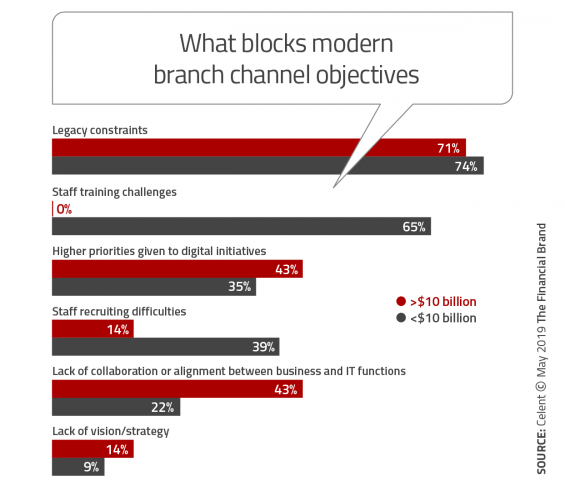

Yet that didn’t show up in the survey. The greatest block among

institutions of all sizes to bringing modern tools to branches was

“legacy constraints.” Among the barriers cited:

Legacy onboarding procedures and systems that tie branch staff to desktop computers and paper instead of working with mobile tablets. (Think of how everything from Apple store receipts to Uber bills gets emailed these days.)

Siloed record systems that prevent frontline employees from understanding the customer journey from end to end.

Administrative tasks that remain manual and which devour time that could be spent more effectively.

Las tendencias de consumo están cambiando, sobre todo a medida que nuevas generaciones de nativos digitales ingresan al mercado

En un contexto social y económico muy complejo,

la industria automotriz aparece como una de las más golpeadas por la

fuerte retracción en ventas. Los números hablan por sí solos: el nivel

de patentamientos se derrumbó 50% en los primeros cuatro meses y nada

indica que las cosas vayan a mejorar en el corto plazo.

Lógicamente,

este mal presente tiene su correlato en otro sector íntimamente

relacionado: el de los seguros. Las firmas tradicionales tratan de

surfear la crisis a como dé lugar. Apuntan a ganar clientes proponiendo

más servicios basados en la incorporación de nuevas tecnologías.

Y

mientras están tratando de acomodarse a esta dura realidad, les cae

otro «baldazo de agua fría»: Mercado Libre, la compañía por lejos más

importante de Argentina en términos de valor bursátil, ya «avisó» que

tiene intenciones de incursionar en esta actividad bajo el formato de

insurtech (insurance and technology).

«Sí, vamos a sumarnos, como ya nos hemos sumado a la industria

fintech», asegura su CEO Marcos Galperín. Sólo basta mirar el los

resultados que obtuvo la compañía cada vez que puso un pie en un sector

para entender por qué el mercado asegurador entró en estado de shock.

El

unicornio ya ostenta una valoración de u$s30.000 millones en Wall

Street. Además, los números su plataforma fintech -Mercado Pago- dan

muestra sobrada de su éxito: procesó más de 3 millones de transacciones

solo en 2018, por un total de u$s17.500 millones.

Galperín quiere ingresar al sector asegurador junto con otras

empresas porque, a su entender, «hay mucho que construir». Claro que

esta construcción la iniciará ofreciendo suculentos beneficios a sus

millones de clientes. Cabe destacar que, en 2018, MeLi Fund, la

aceleradora de Mercado Libre, invirtió tres millones de dólares en la

insurtech 123seguros.

En otras palabras, tiene todo el

caudal de usuarios y la tecnología suficiente como para entrar por la

puerta grande y ser líder en el segmento, quitándoles usuarios al resto.

El premio es por demás atractivo: u$s15.000 millones, que es lo que

mueve la industria. Algo así como el 3% del PBI, si bien aseguran que el rubro tiene potencial para triplicar esa cifra.

«Somos el tercer mercado en América Latina. Operan más de 180

compañías. Nuestro rubro, que mueve unos u$s15.000 millones, podría

expandirse a u$s45.000 millones», asegura el director de Nación Seguros,

Horacio Sánchez Granel.

Más allá del temor que genera el desembarco de Mercado Libre, lo

cierto es que muchas aseguradoras ya están en camino de reinventarse

ante el desembarco de empresas 100% digitales (insurtech) y en el marco

de un entorno con usuarios cada vez más conectados a Internet.

Hoy día, el top 20 de las aseguradoras más importantes del país,

según los últimos datos de la Superintendencia de Seguros, es el que se

muestra en el cuadro a continuación:

Entre este puñado de empresas, todas «tradicionales» y algunas de

reconocida trayectoria, se reparten aproximadamente el 80% del mercado.

Nuevos productos para usuarios exigentes

La llegada de Mercado Libre a la industria esta signada a marcar un

punto de inflexión. La empresa más importante de Argentina -y una de las

más prometedoras del mundo- cuenta con una amplia experiencia en el

sector tecnológico, una caja casi sin límites y la capacidad de generar

una disrupción en cualquier industria en la que se involucre.

En el mientras tanto, las compañías tratan de reacomodarse a un

entorno cada vez más competitivo. «Notamos que el consumidor ahora

tiene otra forma de interactuar al realizar una compra, un trámite u

otro servicio. Por ello, debemos abordarlo diferente», asegura a iProUP Jorge Amadeo, director de Tecnología Informática de La Caja.

Así, ante usuarios cada vez más exigentes, las firmas están obligadas

a dar respuestas rápidas y aportar soluciones con mayor accesibilidad.

Desde La Caja aseguran que el público demanda que las aseguradoras

«hablen en su idioma» para no sentirse burlado por la «letra chica». Por

eso, la firma está trabajando con un nivel lingüístico de fácil

comprensión, sin tecnicismos.

«Hay que repensar los procesos y focalizarse en la transformación.

Más allá de los nuevos productos, hemos cambiado el foco pensando en el

cliente, la autogestión y la facilidad de acceso. Cuando evaluamos

soluciones, partimos de la base que tienen que ser integrales y sumar

agilidad», asegura Eliana Epstein, Head of Digital Seguros de Sura.

La tecnología definitivamente está cambiando la manera en que

la prestación debe ser comunicada y ofrecida. Amadeo aporta un ejemplo

de esta transformación: «Ya se comercializan los productos on/off. Es

decir, el cliente puede decidir cuándo habilitar o deshabilitar una

cobertura».

Las compañías tratan de dar pelea con nuevas iniciativas, acordes a la transformación que experimenta el sector.

Una

de las que está ganando espacio es Klimber, que tiene como uno de sus

acciones principales nada menos que a Grupo Clarín. En octubre lanzó la

marca «Tranqi», junto con Sura, para brindar coberturas para vehículos.

«Operamos con un agente de seguros. Somos los canales digitales de

estas compañías. Trabajamos cada línea con una aseguradora distinta

porque nos permite integrarnos mejor, automatizar procesos y obtener

mejoras en los productos y en los costos», explica Dolores Egusquiza,

gerente de Marketing de Klimber, a iProUP.

La novedad de Tranqi es el «on- off» o «prende y apaga», que le permite al usuario suspender la cobertura durante un tiempo. «Está

pensado para quienes decidan ‘apagar el seguro’ por un tiempo y

reactivarlo luego. Muchos tienen guardado el auto en un garaje o viven

en barrios cerrados y entonces prefieren no tener cobertura», señala la

directiva.

Otro ejemplo es Zurich Now, el primer seguro on demand para

productos tecnológicos: se puede activar y desactivar en 24 horas desde

la app, según la conveniencia y autonomía del usuario, a través de una

experiencia puramente digital y móvil.

En una primera etapa, la firma permite asegurar notebooks,

smartphones y tablets (que la app detecta de forma automática) por una

tarifa diaria. Sin embargo, no sería de extrañar que la empresa anexe

otro tipo de bienes, como los vehículos.

«Zurich Now nace de la necesidad de brindar una solución diferente

para quienes desean protegerse de modo sencillo y 100% digital», asegura

en diálogo con iProUP Mauro Zoladz, Head of Customer Proposition de Zurich Argentina.

Y completa: «Nos propusimos brindar un servicio diferencial a

aquellos que demandaban nuevas formas contratar». En la semana de

lanzamiento, indica que la compañía recibió más de 2.000 pedidos de

cotizaciones diarias por el servicio.

Este tipo de productos acerca a los consumidores al mundo asgurador y

también genera conciencia, al impulsar el control sobre la póliza: días

de uso, costos y monitoreo de la cobertura desde la misma app.

Por su parte, Santander lanzó Seguro de Protección Inteligente

(en conjunto con Zurich) desde su app bancaria móvil que también

protege, en pocos pasos y con algunas fotos, bicicletas, cámaras de

fotos, notebooks, equipos de audio, consolas, entre otros.

También desde La Caja están ampliando la integración de la telemática

a la conducción, para ofrecer a los clientes una cobertura ajustada a

la medida de sus necesidades y nivel de riesgo. De hecho, está

trabajando con un grupo de usuarios que dispone de este producto a

través de sensores en sus vehículos, para así llevar esta solución a la

aplicación.

Otro de los desarrollos de la firma es un asistente virtual basado en

inteligencia artificial. El director de Tecnología Informática de La

Caja explica a iProUP

que el objetivo es «brindar una mejor experiencia. El bot se

desempeñará como asistente de venta y postventa y responderá consultas».

¿Y las insurtech?

Con 16 millones de automóviles en circulación en la Argentina –de los

cuales, más de 13 millones tienen una cobertura–, el segmento de

seguros para vehículos goza de la mayor tasa de contratación del

mercado.

De ese total, las aseguradoras digitales lograron capturar una

porción muy marginal de usuarios. En total, son 11 las firmas que se han

sumado al segmento insurtech. Además, el 50% opera con menos de 10

empleados. Es decir, con costos reducidos y una fuerte apuesta por la

tecnología.

Iúnigo, por caso, posee a la fecha alrededor de 3.000 clientes asegurados según fuentes consultadas por iProUP,

si bien desde la firma aseguran que son poco más de 9.000. La compañía,

dependiente de San Cristóbal Seguros, viene encarando una agresiva

campaña de difusión desde su lanzamiento pero no ha logrado expandirse

más allá de su nicho.

En el marco de la Resolución SSN-219.2018 de la Superintendencia de

Seguros de la Nación (SSN), los controles de tránsito ahora aceptan

cualquier tipo de comprobante digital, lo que permite que estas

inspecciones sean más ágiles. Esto ha significado un verdadero

espaldarazo para el surgimiento de propuestas 100% digitales.

Un mercado prometedor

Sin dudas, la industria de seguros está atravesando un gran momento,

apalancado por las nuevas tecnologías e impulsado por las necesidades de

las nuevas generaciones de clientes.

«Hoy, estamos cruzados por la tecnología y las app. Compramos

productos, pedimos comida, consumimos entretenimiento, planeamos

nuestros viajes, contratamos soluciones para el hogar y proyectamos

nuestra economía familiar desde las pantallas», suma Zoladz.

Al respecto, Epstein de Sura, afirma: «Con prácticas continuas e

iterativas, tenemos que seguir mapeando tendencias y trabajar en

soluciones novedosas para los segmentos con una propuesta de valor

clara». Por eso, es fundamental apoyarse en la innovación.

«Vemos a la innovación como un componente clave ya no sólo para

desarrollar nuevas oportunidades de negocios y mejorar el servicio,

sino como algo esencial para mantener nuestra cartera», finaliza el

vocero de La Caja.

Todo esto ocurre mientras Mercado Libre no está. Cuando haga su debut, las compañías tendrán que afinar aún más sus estrategias para dar pelea en un sector cada vez más competitivo, inclusivo y prometedor.

La transformación digital sin dudas está cambiando el vínculo de los bancos con sus clientes. No sólo desde el lado operativo, por la posibilidad de hacer cualquier tipo de transacción mediante los canales digitales, sino también desde su cara más visible: las sucursales.

El open banking es una de las palancas de transformación de la banca. Supone la entrada definitiva del sector en la era moderna y la colocación del usuario en el centro, dándole el control sobre sus datos. Pero, ¿qué ventajas tiene tanto para los clientes como para los bancos y proveedores de servicios?